On YC startup exits

As a venture capital fund manager, one of the questions I’m asked most often by LPs is “How long will it take to get my money back?”

At Rebel Fund, our job is to invest in the top 5–10% of new Y Combinator startups each year, and in doing so return not only our investors’ initial capital but also earn them a strong financial return over time. Since we typically only return cash to LPs once our portfolio companies achieve an exit (secondary transactions notwithstanding) the purpose of this post is to find exactly how long post-YC it typically takes startups to either get acquired or go public.

In my previous post On 101 Y Combinator unicorns we analyzed the 314 private and 16 public startups on YC’s latest Top Companies list, each now valued at over $150M. However, there are a subset of those 330 startups who have achieved an exit (45 to be exact) and today we’ll take a deeper dive into those stars of investor and founder liquidity.

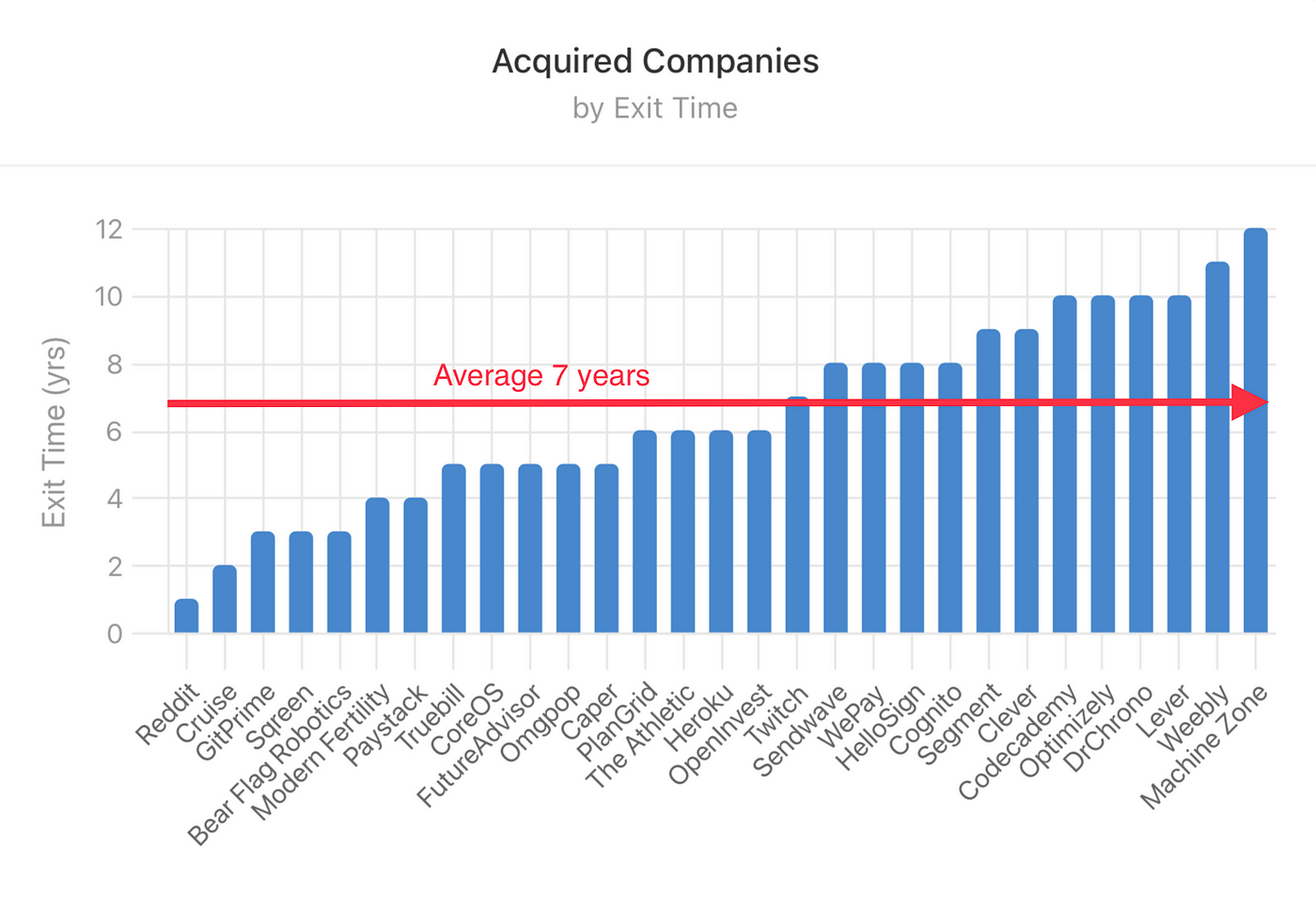

As of now, there are 29 startups on the Top Companies list who achieved an acquisition. While this doesn’t account for all YC startups who have been acquired, it does represent the largest acquisitions which tend to drive the vast majority of investor returns given the steep power law curve of early-stage startup investing.

As you’ll see in the chart below, it took these companies an average of 7 years to get acquired, with a range of 1 to 12 years. These companies have a combined value today of ~$50B. As mentioned in previous posts, early-stage startup investing is only for the patient!

Now moving on to the 16 public YC companies, guess what — we get the exact same 7 year average to achieve an IPO. These companies have a combined value today of ~$130B.

While that answers our most pressing question, let’s dive a bit deeper.

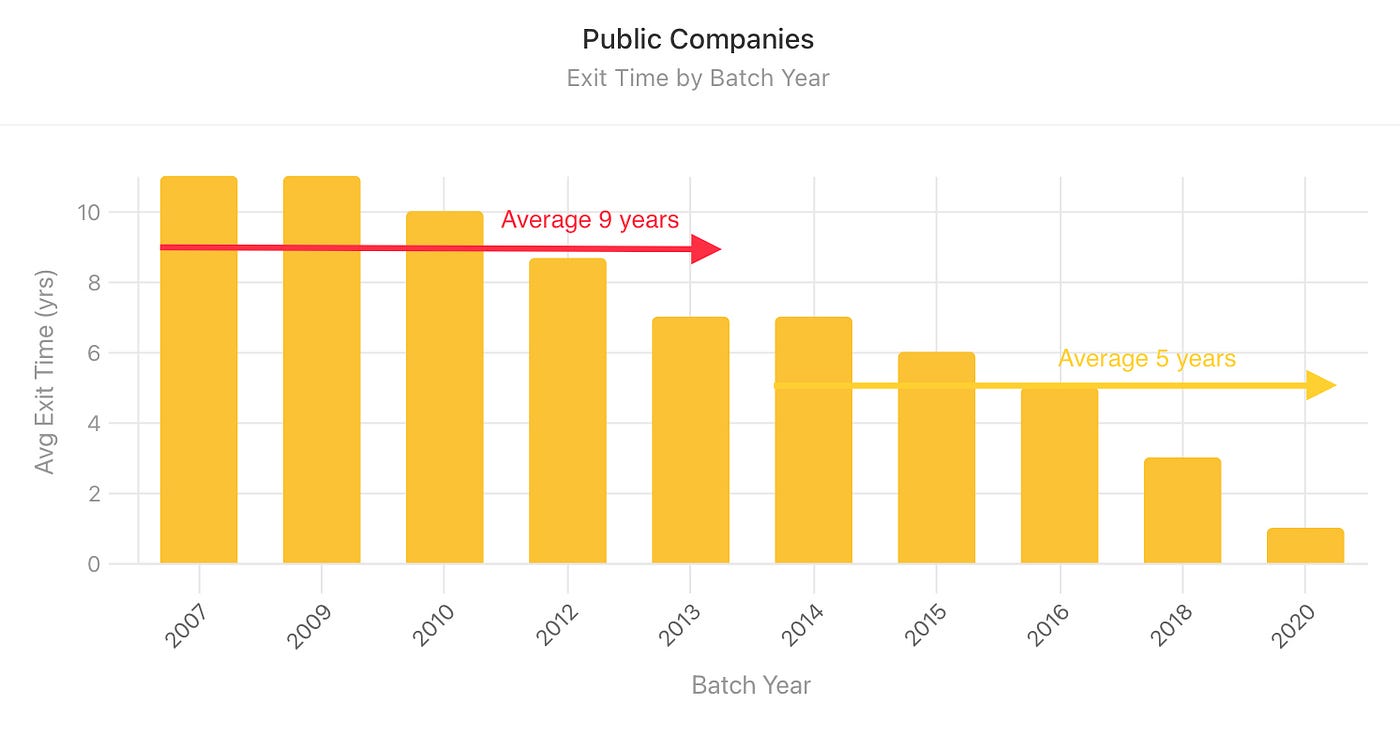

YC has been around since 2005, and a lot has changed over the years. One trend we’ve noticed is the average time it takes YC startups to get acquired has greatly accelerated from 9 years (2007–2012 batches) to 5 years (2013–2018 batches). So, startup investors these days don’t need to be quite as patient as before¹

On the public company front it looks the exact same, with an average 9 years from YC to IPO (2007–2013 batches) accelerating to 5 years (2014–2020 batches).

Both the charts above are somewhat distorted as companies in more recent batches who will exit but haven’t yet should eventually bring up the average exit times for their batch years once they do. However, the general trend of accelerating exit times is undeniable.

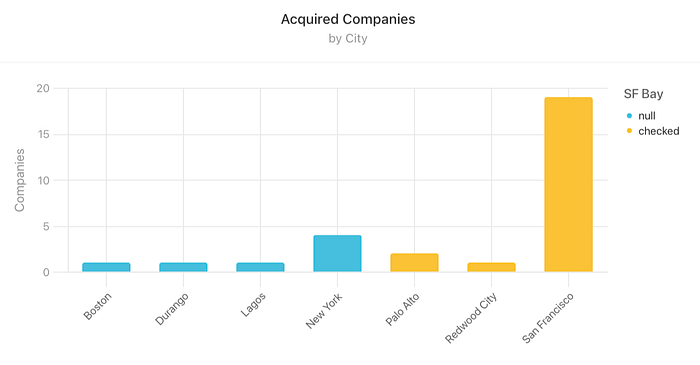

In other recent posts, I’ve pointed to the dominance of Silicon Valley in producing top-performing technology startups (even if said dominance is slowly eroding). We get the message loud-and-clear when looking at the proportion of acquired YC startups that hail from the San Francisco Bay Area — a full 76% of all acquired Top Companies.

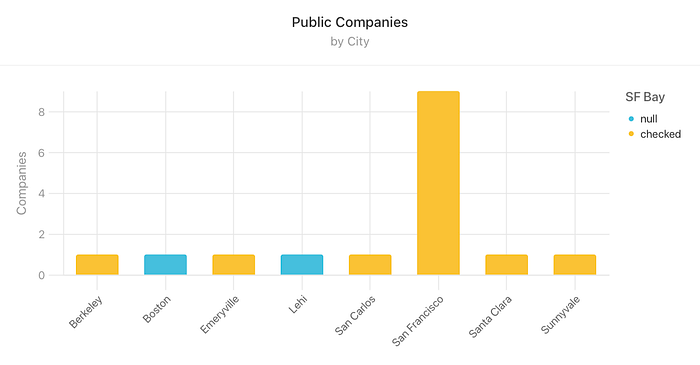

We get the message even louder-and-clearer when looking at the proportion of public YC startups from the SF Bay Area — a whopping 88% of them!

I didn’t even bother charting the proportion of exited startups from the US vs international, as there’s only 1 exited international top YC startup thus far, Paystack in Africa.

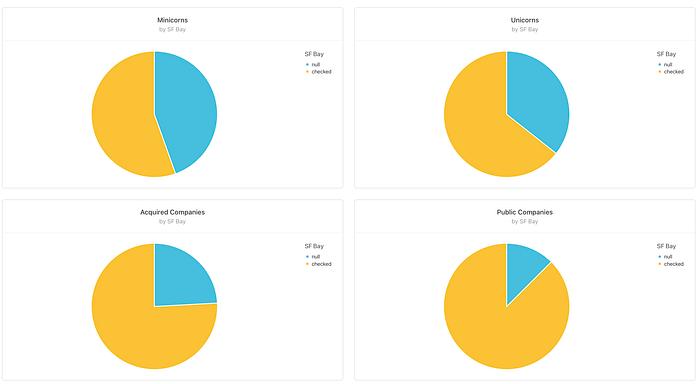

To take this thread even further, if we look at the proportion of minicorn ($150M-$999M valuation), unicorn ($1B+ valuation), acquired, and public YC startups that are headquartered in the SF Bay Area, we can see that Silicon Valley startups become more and more dominant the further they progress on the road to IPO.

I think this speaks mostly to the Valley’s formidable advantages when it comes to capital availability, both in terms of venture capital to grow startups and corporate development capital to acquire them²

That said, before you put all your investment eggs in the Silicon Valley basket, bear in mind that YC has only recently started to rapidly internationalize and I expect many more acquired and public YC startups to emerge from non-US markets in the coming years, particularly developing markets like India, LATAM, and Southeast Asia.

In fact, we’ve observed that some developing markets tend to produce much stronger YC startups than their developed market peers, but perhaps that’s a discussion for another blog post.

¹Maybe the current rising interest rate environment will extend the time it takes for companies to exit, but I’m no macroeconomist so won’t speculate

²The caveat here is that it takes a while for companies to grow into unicorns and even longer to achieve an exit (7 years, as discussed above) so part of the reason SF Bay Area startups are so heavily over-represented in the acquired and public categories is that older YC startups are simply more likely to be from the US and particularly the Bay Area