On 101 Y Combinator unicorns

In August 2022, Y Combinator released its latest Top Companies list, now including 314 private and 16 public YC startups each valued at over $150M. YC officially reported ‘over 80’ of these startups to be valued at over $1B, but our best estimate is there are now 101 Y Combinator-backed unicorns¹.

At Rebel Fund, our job is to invest in the top 0.1% of the tens of thousands of tech startups that apply each year to Y Combinator. We take a very data-driven approach to our investments, collecting and analyzing over 100k data points on hundreds of startups in each new YC batch with our Rebel Theorem 2.0 machine learning algorithm. So, we devote a huge amount of resources to understanding which characteristics tend to drive YC startup success, and the purpose of this post is to share some of our findings.

Earlier this year, I published On $600B of Y Combinator Startup Success and this post is essentially an update. At that time there were 271 startups on YC’s top companies list vs 330 startups today, which is a fantastic achievement. However, we also estimate some major valuation markdowns since that post, which is perhaps why YC didn’t report its total Top Companies’ value this time around.

According to our analysis, the top 10 YC companies lost hundreds of billions in enterprise value since YC’s last Top Companies update in February. Because of this, even with the addition of ~60 new startups to the Top Companies list, we estimate the overall value of YC’s Top Companies may have declined by nearly 30%. The vast majority of this decline came from the large publicly-traded companies, as their valuations respond much more quickly to changes in investor sentiment and drive larger swings mathematically than their privately-traded counterparts.

That said, YC now has more unicorns and $150M+ startups than ever, and my previous prediction that YC startups will exceed $1T in value in the coming years definitely still stands.

So without further ado, I’m glad to share some of our analysis of YC’s latest Top Companies list.

Valuations

As I’ve discussed in the past, startup valuations tend to follow a steep power-law curve and the latest Top Companies are no different.

The 101 YC unicorns account for nearly 90% of all Top Companies’ value, which themselves account for the overwhelming majority of YC’s total portfolio value.

Each of the startups on the chart above are unicorns, and each are incredible success stories for their founders and early investors. Still, the top dozen decacorns dominate the chart, which is what makes early-stage startup investing such a winners-take-all game.

Age

Venture investing is a long-term endeavor, as we can see when we break down YC unicorns by their batch year:

The number of unicorns peaked in the 2016 vintage at a whopping 20 companies, but other years may still catch up as their companies mature.

Another interesting thing to look at is the unicorn rate for each batch year (i.e., the percentage of startups in those batches achieving unicorn valuations) which shows us that while 2016 was a special year at 9%, YC startups tend to average around a 4% unicorn rate overall (ignoring 2019 to present since those vintages are still too young to assess):

If we expand our purview to all YC Top Companies, we can see that 2016 was still special, but the 2018 and 2019 vintages have already surpassed it in number of $150M+ startups. We can also see that YC Top Companies are growing in number more-or-less exponentially over time, bearing in mind the most recent vintages are still maturing:

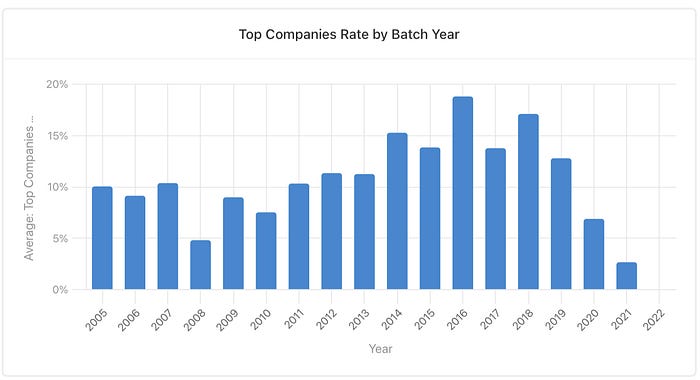

If we look at the Top Companies rate by batch year, we can see that it’s been steadily improving over time (as discussed in On Y Combinator batch quality at scale) and hovering right around ~15% from 2014–2018.

Geography

Most investors have certain geographic targets, constraints or expertise, so it’s important for us to understand which geographic regions YC Top Companies tend to hail from.

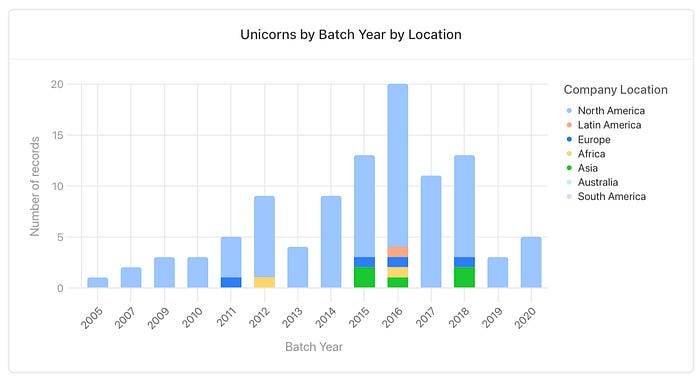

At Rebel, we like to look at unicorn and ‘minicorn’ ($150M-$999M valuation) startups by location by year since YC only started to rapidly internationalize in recent years.

These charts make a few things apparent:

- North America, and particularly Silicon Valley as we’ll discuss below, is responsible for the vast majority of YC unicorns and minicorns

- Part of what made 2016 so special was its international unicorns

- Asia (particularly India) and LATAM are responsible for most of YC’s international success

- International YC startups tend to take longer to mature from Top Companies to unicorns (if they do at all) as evidenced by how much more colorful the minicorns chart is compared to the unicorns chart

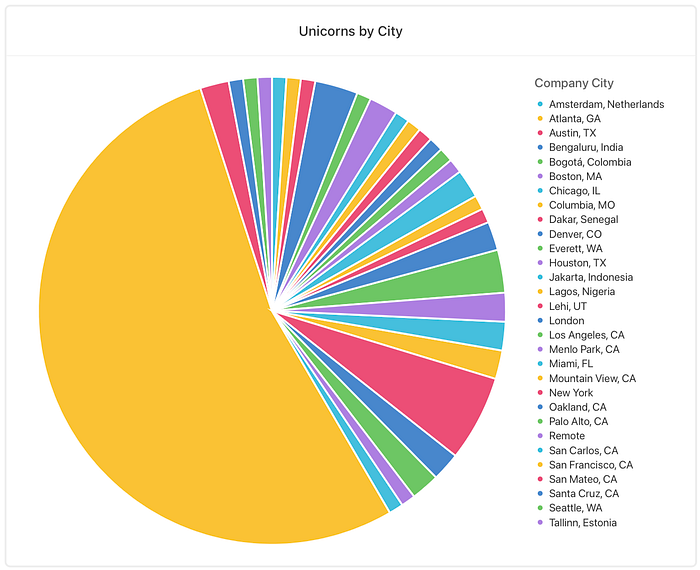

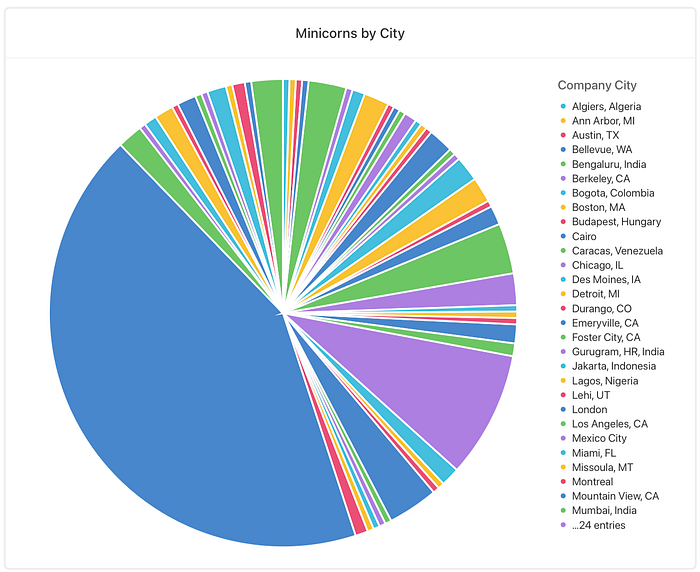

If we break down the unicorns and minicorns by city, more interesting patterns emerge:

The most obvious pattern is that San Francisco dominates both charts, despite the slow erosion of Silicon Valley’s dominance.

However, note that San Francisco dominates the unicorn chart moreso than the minicorns chart. I think this is partially because Silicon Valley startups tend to mature more quickly than their peers (perhaps due to better access to capital) and partially because unicorns take a while to develop and older YC startups are more likely to be from the Valley.

Some cities of note outside of Silicon Valley are:

- New York (6% of unicorns and 9% of minicorns)

- Los Angeles (3% of unicorns and 4% of minicorns)

- Bengaluru, India (3% of unicorns and minicorns)

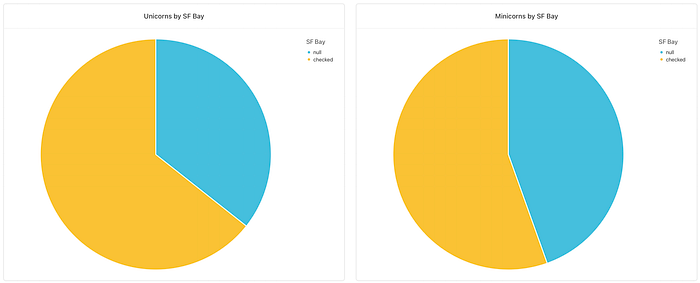

Speaking of Silicon Valley, once we include the Bay Area cities besides SF that comprise it, we can see the Valley’s dominance even more clearly:

A whopping 64% of YC unicorns and 55% of YC minicorns are from the SF Bay Area. Founders and investors take note :-)

Industry

If we look at unicorns and minicorns by industry side-by-side, we can see clearly which startup technology sectors are most up-and-coming:

Here we can see the continued dominance of the B2B Software & Services sector, as I’ve discussed in previous posts. However, there are less minicorns (45%) than unicorns (54%) in this sector, which predicts that future unicorns may come disproportionately from other sectors.

Some other industry findings:

- Financial technology (aka ‘fintech’) is the second most dominant sector (21% of unicorns and 16% of minicorns)

- Consumer is the third most dominant unicorn sector (8%) but healthcare beats it out for the minicorns (9%)

- The major new emergent sectors for the minicorns are machine learning (8%) and marketplace (7%), so I’d expect to see disportionately more unicorns in these sectors in coming years

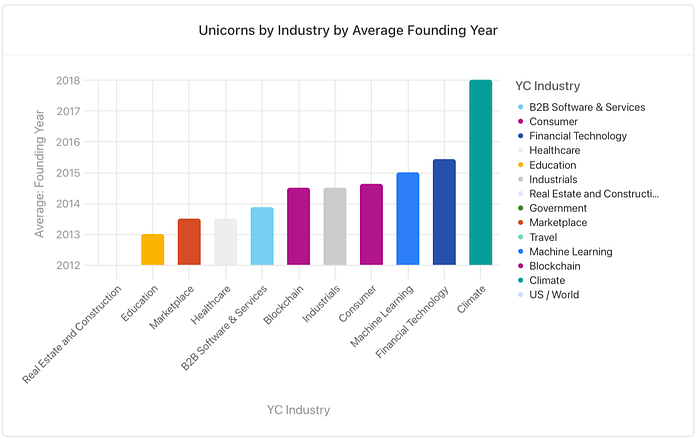

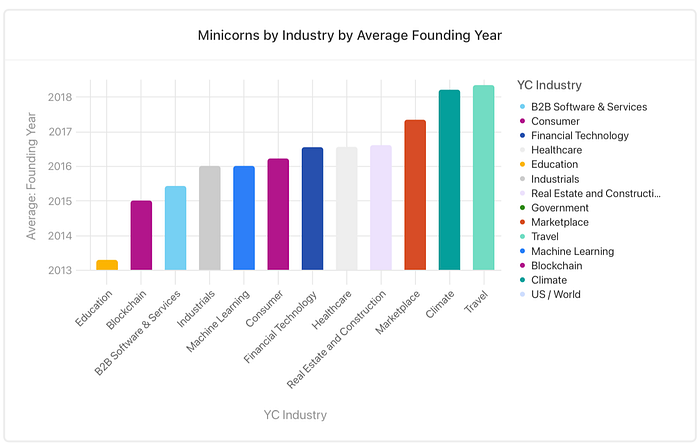

Another way to look for industry trends in the YC startup world is to examine unicorns and minicorns by industry by average founding year (which may be different than their batch year)

Here we can see that the ‘younger’ unicorns are more likely to be in climate, fintech, and machine learning, and the ‘older’ unicorns are more likely to be in real estate, education, and marketplace (the latter of which is also emergent in the minicorns, so maybe it’s coming back into fashion)

When we look at the minicorns by industry by average founding year, the ‘younger’ ones are more likely to be building in the travel, climate and marketplace sectors, and the ‘older’ ones in education, blockchain (interesting…) and B2B.

Conclusion

While no amount of data analysis can replace the trained eye of an experienced investor, it’s a useful way of overcoming individual biases and understanding objectively which factors tend to be correlated with YC startup success.

Taken as a whole, these charts tell me that the best sectors to watch as an investor right now are climate, fintech, machine learning and marketplace, plus of course the ever-popular B2B. The geographies to watch, in addition to the perennial powerhouse that is Silicon Valley, are probably emerging markets like LATAM and South Asia, plus NYC here in the US.

Most of all, this data tells me to go long on Y Combinator startups overall, as 101 YC unicorns is no small feat 🎉

¹Since the value of most Y Combinator startups is private, we estimate valuations based on latest announced funding rounds and the order in which they appear on YC’s Top Companies list