On $600B of Y Combinator Startup Success

Last year I published a popular blog post On $300B of Y Combinator Startup Success that analyzed YC’s Top Companies list that year, which included 137 portfolio startups with a combined valuation of over $300B.

YC recently published an updated Top Companies list including 271 companies with a combined official valuation of over $600B (we now estimate it closer to ~$900B). Much can change in a year!

At Rebel Fund, our job is to invest in the top 0.1% of the 30,000+ tech startups that apply each year to Y Combinator, the world’s #1 technology startup accelerator. We take a data-driven approach to our investments, collecting and analyzing over 100k data points on the 400+ startups in each new YC batch. We maintain what I believe to be the most comprehensive dataset of YC startups and founders that exists outside of YC itself.

Each year we analyze YC’s Top Companies list to gleam insights on the factors leading to YC startup success, to improve our Rebel Theorem machine learning algorithm and just keep top-of-mind as we meet with founders. The goal of this post is to share some of those insights.

Valuations

As with last years’ post, I’d like to start by emphasizing just how incredibly skewed value creation is in the world of tech startups. Startup valuations tend to fall along a steep power law curve in an eerily predictable way.

There are over 3,000 YC startups today but only 60+ unicorns according to YC’s official statistics (we now count closer to ~90). These unicorns account for over 95% of all YC startups’ value!

Even amongst the unicorns, just a few dominate. According to our math, the top 10 YC startups alone have a combined valuation of over $600B. This chart illustrates how even in the unicorn club, it’s winners-take-all:

There’s a reason venture investors are so obsessed with ‘unicorn catching’ — they really do drive portfolio returns. At Rebel, we’ve already made some unicorn investments in our last couple years of seed-stage investing, with these companies each driving over 100x gross markups for the fund — and they’re still growing fast.

Age

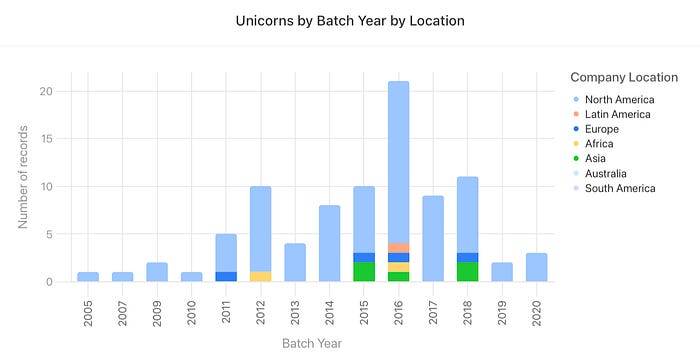

Venture investing rewards the patient, as it typically takes 5–10 years for a technology startup to mature. When we analyze YC’s top companies by batch year, we can see the unicorns tend to be 5+ years old:

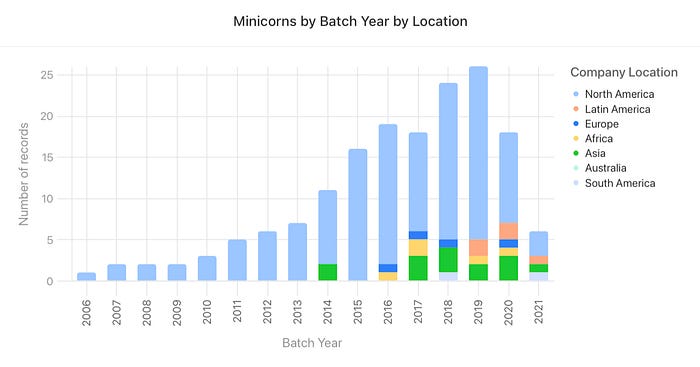

However, the ‘minicorns’ (companies valued $150M — $999M) are often much younger since it doesn’t take as long to grow into that valuation range:

You’ll notice that the unicorn count peaks in the 2016 batch and minicorns peak in the 2019 batch. This does not mean that YC’s best days are behind it, but rather that more recent batch startups are still maturing.

You’ll also notice the exponential rise in minicorns from 2006–2019, which I believe is a function of both increasing YC batch sizes and improvements in YC’s selection process and overall effectiveness as an accelerator.

To provide some context, YC had 32 unicorns from its 2012–2015 batches out of 616 companies in those batches — a 5% unicorn rate. Something special happened in 2016, which had 21 unicorns out of 226 startups — a whopping 9% unicorn rate! The more recent years are too soon to call, but given YC’s current ~400 company batch sizes and ever-improving batch quality, I wouldn’t be surprised to see 20+ unicorns per batch eventually develop from recent vintages.

Region

So where do all these unicorns and minicorns come from?

We can visualize the answer by looking at the charts above with a company location overlay:

It’s clear that North America dominates both charts, mostly because YC has historically had a bias towards North American (predominantly US) startups in their admissions process. Almost all of the unicorns prior to 2015 were from North America, though we start seeing a bit more color in the 2015 and 2016 bars.

Where we really see YC’s internationalization efforts paying off is the younger minicorn chart, which has a significant minority of international startups starting in 2017.

We’ve also found the proportion of international minicorns from recent batches starting to reflect the overall international startup rate of their batch: From 2019, ~20% of the minicorns are international out of ~40% international companies in those batches, but from 2020, ~40% of the minicorns are international out of about the same proportion of international startups in those batches.

Anecdotally, we’ve noticed the international YC startups tend to be further along than their North American peers in terms of revenue traction, age, founder experience, etc. However, they’re still at a disadvantage in terms of valuation growth, which may be simply because their local funding environments are less mature.

City

A couple years ago I wrote about the slow erosion of Silicon Valley’s dominance when it comes to tech startups, and since then both the Valley’s dominance and its slow erosion have continued, which we can see in these breakdowns of the unicorns and minicorns by city:

In each pie chart, it’s easy to see the San Francisco Bay’s dominance (blue and then green — sorry for the color change). However, since the minicorns are younger, they’re less likely to be based in the Bay Area than the unicorns (57% of minicorns vs 65% of unicorns).

The cities taking the biggest bites out of Silicon Valley’s dominance are New York (9% of minicorns), Los Angeles (4% of minicorns), Boston & Bengalura, India (each 3% of minicorns). While the charts above don’t capture it, we’ve also noticed a huge portion of YC startups lately that are remote-first, making their physical location less relevant.

Industry

A couple years ago I also wrote about the shifting landscape of YC batches by industry, and many of the trends I spoke about have continued, with some new trends starting to emerge as well. Let’s look first at the unicorns broken down by industry:

B2B dominates, as it always has with YC, despite popular opinion. Financial technology (aka ‘fintech’) produces massive value as well, with YC unicorn startups like Stripe & Brex as good examples.

Things get more interesting when we compare the pie chart above to the minicorn breakdown by industry:

Now it’s clear that things are shifting with the younger minicorn companies. While B2B and fintech are still the dominant sectors, they’re losing share to healthcare (10% of minicorns), machine learning (8% of minicorns), and marketplace (7% of minicorns).

Also notice the tiny emerging slice for climate (2% of minicorns). While this emerging sector is certainly important, it’s still a much smaller proportion of minicorns than many would expect — the hype curve in action perhaps?

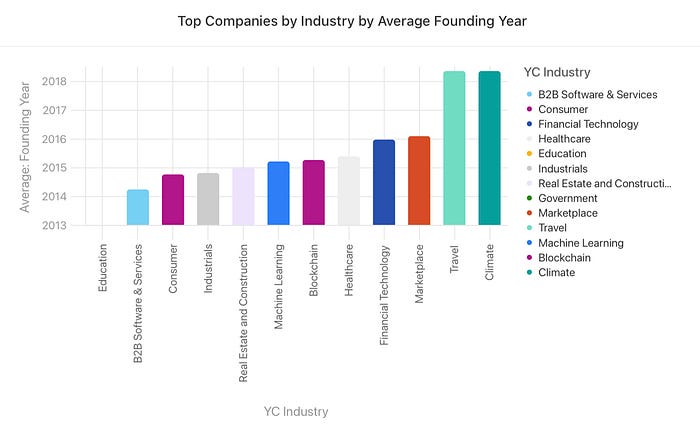

Another way to look at sector trends is analyzing all top companies (unicorns + minicorns) by industry by average founding year:

Here we can see that climate and travel startups tend to be the youngest, but I wouldn’t look too much into the latter since there are only a few travel companies in the top companies list.

More notably, we can see that education, B2B, and consumer companies tend to be the oldest, and fintech, marketplace, and healthcare companies tend to be the youngest (besides aforementioned climate and travel). These sectors are also well-represented in terms of volume, so investors should keep a close eye on them.

These are just a taste of the insights we can gleam from analyzing tens of thousands of data points on hundreds of top YC startups. In my next post, I’ll talk about a few of the trends our recently updated Rebel Theorem machine learning algorithm picked up when comparing the characteristics of top-performing YC startups and founders to their peers.