On the last decade of Y Combinator

Since taking my last startup through Y Combinator as a founder over a decade ago, I’ve had the privilege of attending every YC Demo Day since my own in 2013 and investing in every YC batch professionally since 2018. It’s been fun to watch YC grow and evolve over the years, transitioning from Paul Graham’s leadership (2005–2014) to Sam Altman’s (2014–2019) to Geoff Ralston’s (2019–2022) to Garry Tan’s (2023-present). YC has really come into its own as an institution and had an enormous impact in Silicon Valley.

At Rebel Fund, we’re positioned to be the single largest supporter of YC startups at the seed stage, now with close to $200M committed to invest in YC startups across our various funds, and portfolio companies nowvalued at over $12B in aggregate and growing. As an extremely data-driven fund entirely focused on the YC ecosystem, we’ve also built the world’s largest database of YC startups and founders outside of YC itself, now with millions of data points on thousands of companies, which puts us in a great position to track YC startup trends over time.

This post will highlight some of the trends we’ve discovered in YC companies and founders over the past decade through the lens of our data.

Companies

I’ll start with the most easily observable trend — number of companies by batch year. YC had been ramping up batch sizes steadily since 2015, but it really accelerated in the Covid / ZIRP years, in part because the program went 100% virtual. Lately things have settled at around 500–600 startups per year, though I expect this number to start growing again soon thanks to the AI revolution and YC moving from 2x to 4x batches per year.

Whenever I mention YC’s growing batch sizes to LPs, the immediate question they ask is some version of “Don’t you worry that the quality of YC startups is getting diluted?”

This concern is amplified by the fact that most of YC’s most famous and valuable startups were founded many years ago, giving the impression that YC’s best days are behind it. Our own data indeed shows a downward trend over the past decade in the proportion of YC startups that have been acquired or gone public, and those that have achieved unicorn ($1B+) or top companies ($150M+) valuations:

Of course, what these charts fail to take into account is it takes 7 years on average for a YC startup to achieve an exit, so naturally the most successful startups were founded a long time ago.

The good news is every leading indicator of YC batch quality that we track at Rebel continues improving over time despite growing batch sizes, from YC application acceptance rates to fundraising progress to founder quality metrics. So, we believe YC’s future success will far outpace the outcomes it’s achieved thus far.

The composition of YC batches has also evolved over time. While B2B startups have always been a mainstay, consumer companies have definitely fallen out of favor in recent years, and fintech experienced a resurgence in the ZIRP years (logically). In the last couple of years that have kicked off the AI revolution, B2B is stronger than ever, as AI-native vertical SaaS and dev tool startups are creating huge opportunity for founders and investors.

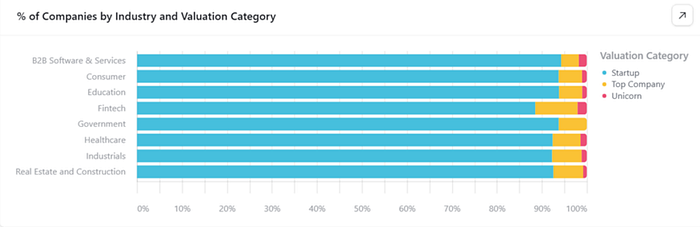

All technology sectors are not created equally though — our data shows that it’s much easier to build a top company or unicorn in some areas than others. Fintech is a standout on the ‘easier’ side, and apparently it’s impossible to build a unicorn serving the Government 🤔

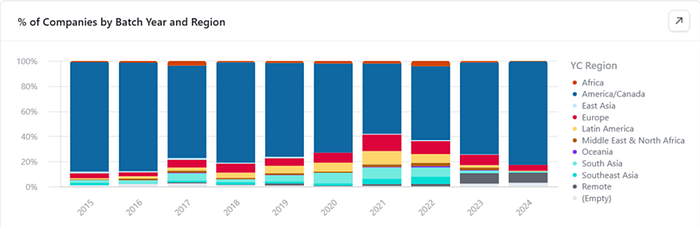

YC startups have also waxed and waned by geography. In the early years, YC was almost entirely US-focused, but it became much more receptive to international startups (particularly from emerging markets) during the Covid / ZIRP years, but has recently refocused squarely on the US and other developed markets. My guess is YC partners saw the same trend in their data that Rebel saw in ours… the closer a startup gets to Silicon Valley, the more likely they are to become a unicorn.

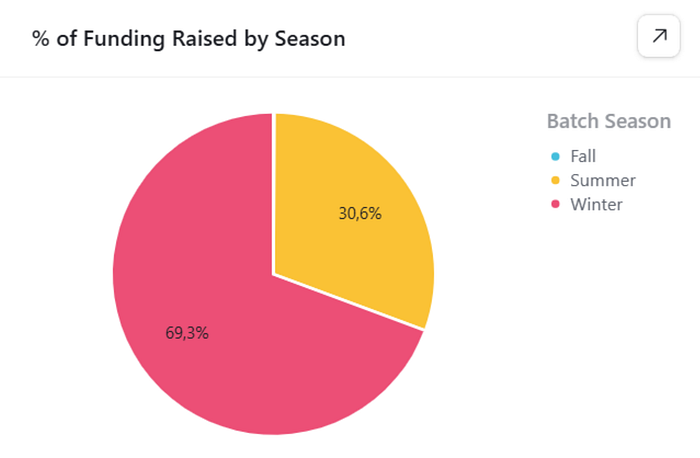

An interesting quirk we noticed is that YC’s Winter batches (January — March) seem to outperform its Summer batches (June — August). The Winter batches are about ~10% larger on average, but notably, they raised nearly 70% of all the capital! Maybe in the summertime, VC’s are too busy galavanting across Europe, kitesurfing in Puerto Rico, or partying at Burning Man to invest in startups (those who know me will appreciate how self-deprecating that was 😂)

Founders

YC startups are nothing without their founders, and since founder quality is the #1 factor we underwrite at Rebel, the vast majority of data we collect and feed into our Rebel Theorem 3.0 machine learning algorithm is founder-related. There are lots of trends I could speak to regarding YC founders, but here I’ll highlight a few of the more interesting ones.

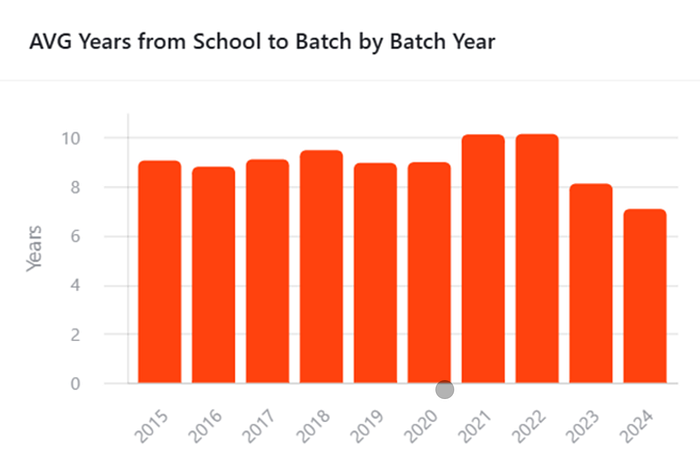

Let’s first talk about YC founders’ age, which we don’t track explicitly at Rebel, but can infer by how many years passed between when they started college and their YC batch (we used to look at years since they finished college, but realized that doesn’t account for dropouts). The chart below shows “school to batch” historically averaged around 9 years, which implies an average YC founder age of 27, assuming they started college at 18.

What’s interesting is average YC founder age has reached historic lows in the past couple of years, hitting around 25 years in 2024. I believe this is a direct result of the AI revolution — since generative AI is such a new technology, younger founders are at no disadvantage understanding and building around it, so YC batches are trending younger.

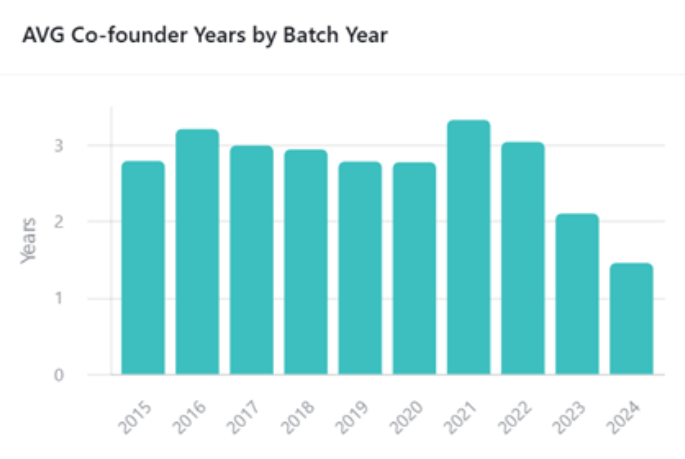

Another way we look at YC founder experience at Rebel is how many years of experience founders had as a startup co-founder. Here we see an even sharper drop-off in the last couple of years, with average co-founder experience hovering around 3 years for the most of the past decade, but declining to half of that last year. The most recent cohorts of mostly AI-focused YC founders are much less experienced as startup founders.

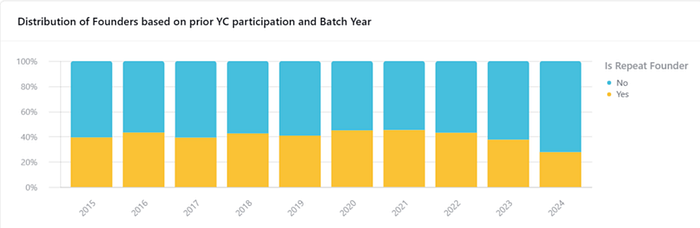

They’re also much more likely to be first-time founders…

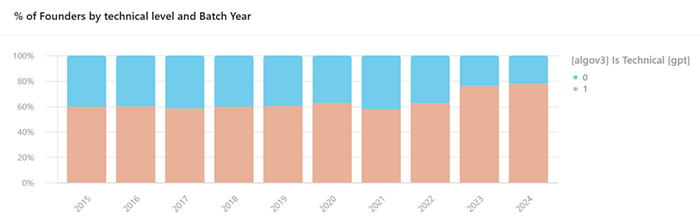

…and much more likely to be technical:

The YC founder characteristics we’ve covered so far are relatively straightforward and easy to measure. However, we also look at some less obvious founder characteristics at Rebel, like founder personalities types as assessed by their online footprint using AI.

The biggest shift we’ve noticed is that YC founder Dominance and Influence personality traits have decreased dramatically over the past couple of years, which makes sense given how much younger and more technical the founders are these days.

These younger and more technical founders are more likely to display Steadiness and Conscientiousness personality traits, which also goes with the “nerdy engineer” stereotype.

There’s a lot more I could say about YC founder personality traits, how we measure them at Rebel, and how predictive they are of startup success, but I’ll save that for another blog post.

YC startup and founder profiles have and certainly will continue to evolve with the changing technological and macroeconomic landscape. You can probably infer a lot about the broader technology world by looking at these YC trends as well, so I hope you’ve found at least some of these insightful!